In today's investment environment, precise terminology is becoming a strategic imperative. We often see the terms sustainability, social responsibility, and ESG (Environmental, Social, and Governance) merging. into a vague whole, leading to serious errors of interpretation. For the financial analyst, this confusion poses the risk of mispricing assets. The distinction between whether a company is mitigating its impact on the world or merely managing environmental risks to protect its own returns (financial materiality) is a cornerstone of modern investment analysis.

1. Conceptual Framework: Distinguishing CS, CSR and ESG

For an in-depth understanding of the ESG ratings market, it is essential to precisely define four key terms that shape the current discourse on sustainable business.

| Concept | Definition | Main dimensions | Primary goal |

| Corporate Sustainability (CS) | Corporate actions supporting prosperity, social equality and environmental integrity. | Economic, social and environmental | Identify and mitigate sustainability impacts and their interrelationships. |

| Corporate Social Responsibility (CSR) | Corporate actions supporting moral and socially responsible behavior. | Social (often also includes environmental) | Identify and mitigate social harms or irresponsible behavior in society. |

| Environmental, Social, and Governance (ESG) | A set of factors (E, S, and G) that can materially affect the value of a business. | Environmental, Social and Governance | Identify risks and opportunities for the company's financial performance (economic factors are the output of the analysis). |

| Sustainable Development Goals (SDGs) | A global framework of goals for securing a sustainable future by 2030. | Environmental, social, economic and governance | To highlight urgent global challenges and ensure a sustainable future at a societal level. |

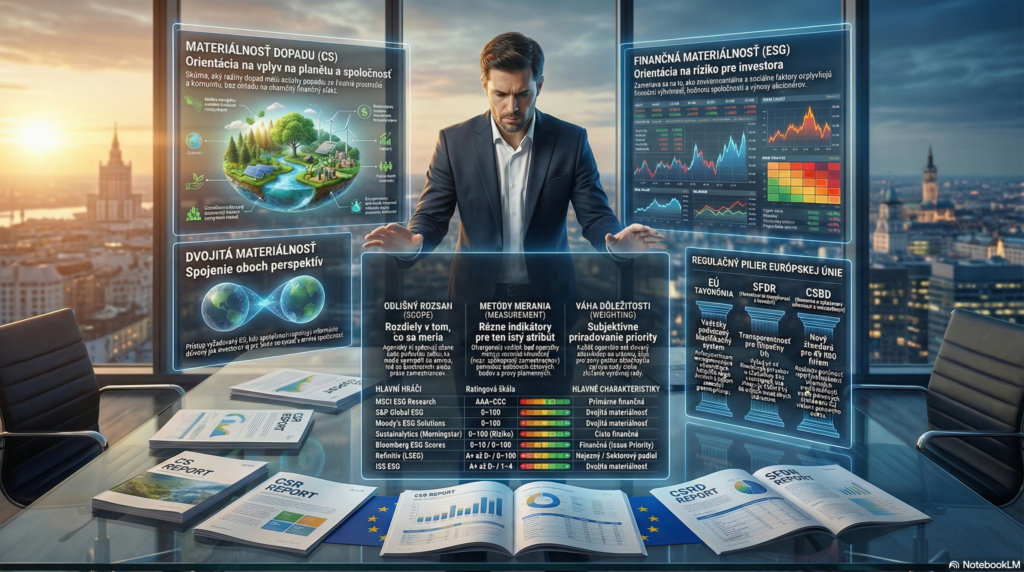

„"So What?" layer: The shift from CS to ESG represents a paradigmatic shift. While CS focuses on the impact of the company on the world (sustainability as outcome), ESG focuses on the impact of the world on the company (financial performance as outcome). The critical point is that within the ESG construct, the economic dimension is absent as an intrinsic element – it serves exclusively as an objective of financial analysis. This shift towards financial materiality transforms environmental factors from ethical choices to critical inputs into risk assessment. This conceptual anchoring is essential for understanding the regulatory pressure in the EU.

2. Regulatory Catalyst in the EU: From Voluntary to Mandatory Transparency

Through the "Action Plan for Financing Sustainable Growth", the EU is transforming ESG reporting into a standardized discipline with the aim of reorienting capital and preventing greenwashing.

- NFRD (Non-Financial Reporting Directive): Valid since 2018 for large entities (over 500 employees). Although a milestone, it suffered from excessive flexibility and low data comparability, as it allowed companies to choose from multiple inconsistent frameworks.

- SFDR (Financial Services Disclosure Regulation): From 2021, it imposes obligations on financial advisors and market participants to increase product transparency and reduce the risk of greenwashing in portfolios.

- EU Taxonomy: A science-based classification system defining environmentally sustainable activities. It sets clear criteria for six environmental objectives, reducing market fragmentation.

- CSRD (Corporate Sustainability Reporting Directive): A direct response to the shortcomings of the NFRD. It expands its scope to approximately 49,000 companies, introduces mandatory audit (assurance) of information and a digital data format. The key role here is played by EFRAG, the institution responsible for creating binding European reporting standards.

„"So What?" layer: The central concept is „Double Materiality“. It distinguishes between financial materiality (the impact of climate on the value of a company) and environmental/social materiality (the impact of a company on the climate and society). This dualism is crucial: a company can no longer be considered sustainable simply because it manages its financial risks effectively if its operations negatively impact biodiversity or human rights. While regulation creates the framework, the ratings market has undergone its own evolution towards concentration.

3. Market Dynamics: Concentration and profiling of major players

The ESG ratings market has evolved from niche agencies to dominant financial clusters. This consolidation is integrating ESG data directly into mainstream financial terminals.

- MSCI (MSCI ESG Research): A dominant player that built its methodological legacy through the acquisition of key companies KLD, Innovest and RiskMetrics.

- S&P Global: It integrated Swiss RobecoSAM (CSA survey) and Trucost (environmental data).

- Moody's ESG Solutions: It was formed through the acquisition of European leader Vigeo Eiris and physical risk specialist Four Twenty Seven.

- LSEG (London Stock Exchange Group): It controls Refinitiv (formerly Asset4) and FTSE Russell.

- Morningstar: It owns Sustainalytics, thereby linking ESG analysis with retail investing.

- Bloomberg: A private giant using both its own data and strategic partnerships.

- Deutsche Börse: It absorbed the agency ISS ESG (which previously acquired Oekom Research and Ethix SRI).

„"So What?" layer: Consolidation has increased professionalism and data availability, but it also raises questions about independence. Integration into large financial houses leads to the dominance of a purely financial view of sustainability. ESG becomes a product for maximizing returns, which can suppress the original systemic view of sustainability (CS).

4. Comparative analysis of methodologies: 8 pillars of ESG assessment

Behind a single letter rating lies a complex hierarchy of data and analytical judgments. Below is a methodological comparison of eight key agencies.

Table A: Data sources and level of company involvement

| Agency | Data access | Company Engagement | Specific element |

| S&P Global | Questionnaire (CSA) + public sources | Active (questionnaires and meetings) | Independent 3rd party verification |

| Moody's | VE Connect + public resources | Active involvement of companies | Analysis of FACTIVA press materials |

| Refinitiv | Exclusively publicly reported data | No questionnaires | Percentile score (percentile rank) |

| MSCI | Public sources + NGO databases | Verification, no questionnaires | Weekly monitoring of controversies |

| Sustainalytics | Public data + 3rd party research | No active involvement (feedback only) | 1,300 data points per company |

| Bloomberg | Direct public sources only (primary) | Only when correcting errors in disclosure | Disclosure Factor (weighted by transparency) |

| FTSE Russell | Publicly available information | Verification via web platform | Threshold bands |

| ISS ESG | Public sources + NGO/Gov data | Annual feedback invitation | Norm-based assessment |

Table B: Materiality and categorization of outputs

| Agency | Materiality type | Aggregation method / Weight | Rating scale |

| MSCI | Financial | Industry Adjusted Score (IAS) | AAA to CCC |

| Sustainalytics | Financial (Risk) | Unmanaged Risk (Beta multiplier) | 0 – 100 (Risk categories) |

| S&P Global | Double | Statistical correlations with ROA/ROE | 0 – 100 |

| Moody's | Double | Leadership/Implementation/Results | 0 – 100 |

| ISS ESG | Double | 12-point scale / Prime Status | A+ to D- |

| Refinitiv | Unclear (Sectoral impact) | Magnitude weights (deciles) | 0 – 100 / A+ to D- |

| Bloomberg | Financial | p-mean (generalized average) | 0 – 10 |

| FTSE Russell | Financial | Combination of Exposure and Score | 0 – 5 |

„"So What?" layer: A critical example of methodological divergence is the approach MSCI to the company McDonald's. Although the company produced more emissions than the entire country of Portugal, MSCI upgraded its rating. The reason was to completely exclude carbon emissions from the calculation because analysts judged that climate change did not pose an immediate financial risk to shareholders' profits (idiosyncratic issues). In contrast, dual materiality agencies (S&P, Moody's) would penalize this fact due to the systemic environmental impact.

5. Challenges and recommendations for professionals: Why do ratings differ?

Relying on a single „black box“ rating without understanding the context is strategically risky. According to Berg et al. (2019), there are three main sources of divergence:

- Measurement Divergence: Largest contributor; different indicators for the same attribute (e.g. different metrics for diversity).

- Scope Divergence: Rating agencies measure different sets of attributes.

- Weights Divergence (Weights): Different opinions on the relative importance of attributes.

Added to this is „"rater effect"“, where the analyst's subjective perception of the company influences scores across categories, and the transparency paradox, where more disclosure leads to greater differences in ratings due to the need for subjective judgment about their quality.

Recommended "Best Practices":

- Diversification of resources: Combine ratings with financial materiality (MSCI) and dual materiality (S&P, ISS).

- Raw data analysis: Track individual indicators, not just an aggregate number.

- Controversy scores: These indicators capture incidents (e.g. data breaches, scandals) faster than the annual update of the overall score.

- "Manageable risk factor" check: Distinguish between risk that the company can influence and systemic risk.

The future of ESG in the era of standardization

We are on the threshold of a new era, where regulations like the CSRD have the potential to bring order to the „methodological wild west.“ Harmonizing reporting through EFRAG will reduce the scope for subjective guesswork and increase the quality of input data.

Although methodological divergence persists, a move towards measuring real impact is essential to achieving the goals of the Paris Agreement. Financiers must realize that ESG ratings are not a goal, but a tool. Quality analysis will always require critical human interpretation, able to see beyond a single number and understand the real relationship between business and the world. The role of the EU Taxonomy in reducing this uncertainty will be a key stabilizing element in the market in the coming years. JRi&CO2AI

Source: Document from the European Commission's Joint Research Centre